As a consequence of the impact of the coronavirus crisis Germany’s government has decided on March 10, 2020 to facilitate access to the Short-Time Work Allowance by government decree. The government decree has not yet been issued, but it shall become effective as of the beginning of April 2020 until the end of 2021.

What is Short-Time Work exactly?

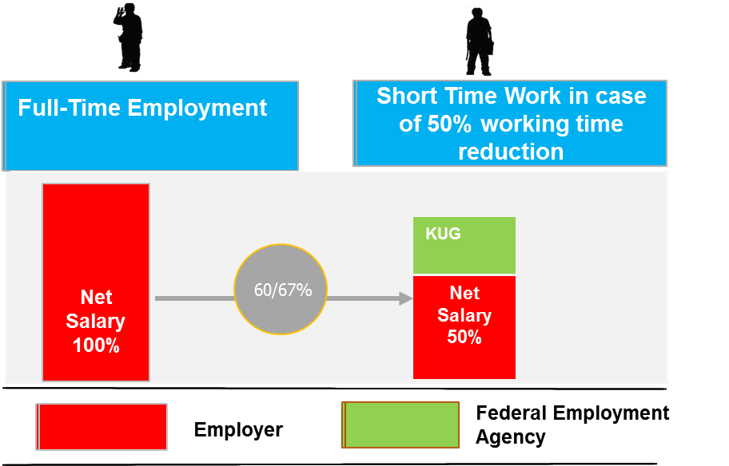

Short-Time Work is the temporary reduction of working hours for a limited period of time in the business operation or selected organizational units. This allows employers to significantly reduce personnel costs in times of crisis with the purpose to avoid redundancies.

In case the working time is e.g. reduced to 50%, the Employer pays 50% of the employee’s salary. The Federal Employment Agency pays a Short-Time Work Allowance (KUG) amounting to 60% (67% for employees with children) of the so-called lost flat-rate net salary. This leads to a significant reduction of labor costs for employers due to the reduction of working time and remuneration in case of temporary economic difficulties. The salary reductions for employees are made up for by the government to a certain extend and for a limited period of time by payment of the Short-Time Work Allowance. The working time can be reduced up to 0 working hours.

General Preconditions for Short-Time Work

In order to qualify for short time working allowances, the following conditions must be met:

- The employer must face a significant reduction of work based on economic reasons or an unavoidable event. Economic reasons can be any reasons in connection with the economic situation, such as lack of goods, reduction in sales, organizational changes based on the economic development. Measures outside the employer’s responsibility, such as site closures by authorities or the interruption of delivery chains due to corona as well as natural disasters constitute such unavoidable events.

- The triggered reduction in work must be temporary, i.e. based on the individual circumstance a return to full-time work must be foreseeable with a certain probability.

- Furthermore, the reduction of work must be unavoidable. It is not unavoidable, if it is typical for the industry sector, if it is seasonal, or if it is solely based on internal organizational measures. The reduction or dissolution of credits on working time accounts is no longer required to avoid the reduction of work.

- At least 10% of the employees in the business operation or department must be affected by the reduction of work in the respective calendar month and therefore suffer from a salary reduction of at least 10%. This covers all employees who are obligated to pay social security contributions including fixed-term employees.

Personal Preconditions for Employees

To be eligible for Short-Time Work Allowance, employees must meet personal preconditions:

- The employee must continue an employment subject to social security after the work time reduction.

- Furthermore, short-time working allowance can only be granted, if the employment has neither been terminated by dismissal, resignation or mutual termination agreement.

- Employees who have reached the statutory retirement age or who are on long-term sick leave (with sick allowance) are also excluded.

Additional Preconditions

In addition the following conditions must be met:

Short-Time Work must be agreed with the works council (if any exists) and cannot be implemented unilaterally by the employer. In businesses without a works council, Short-Time Work must be agreed individually or implemented by so-called dismissal with the offer to continue the employment under modified conditions.

The Federal Employment Agency must be notified in writing of the implementation of Short-Time Work.

Short-Time Work Allowance – KUG

If the afore preconditions are met, the Federal Employment Agency pays a Short-Time Work Allowance in order to compensate the employee partially for the loss of salary. The Allowance amounts to 60% (67% for employees with children) of the so-called lost flat-rate net salary. It is paid tax-free. The employees remain covered by health care and pension insurance during Short-Time Work.

The Short-Time Work Allowance is capped. Only the gross salary up to the contribution assessment ceiling for pension and unemployment insurance can be used for the calculation of the Short-Time Work Allowance. This ceiling is EUR 6,900 in the former western (including Berlin-West) and EUR 6,450 in the former eastern part of Germany.

Social Security Contributions on the reduced salary are shared between employer and employee but Social Security Contributions on 80% of the difference between the regular salary (without Short-Time Work) and the reduced salary are to be borne by the employer. A reimbursement in the amount of 50% by the Federal Employment Agency is planned, but subject to certain conditions (training of the Employee during Short-Time Work).

Supplements by the employer to the Short-Time Work Allowance are possible. They are subject to income tax, but not to social security if the supplement and the Allowance do not exceed 80% of the difference between the regular (full-time) salary and the reduced salary.

Currently, the Short-Time Work Allowance can be paid for a maximum of 12 months.